U.S. SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

| þ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the Fiscal Year Ended December 31, 2014

| ☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from ________________ to ________________

Commission File Number 001-34048

| NEXT GRAPHITE, INC. |

| (Exact name of registrant as specified in its charter) |

| Nevada | 90-0911609 | |

| (State or other jurisdiction | (IRS Employer | |

| of incorporation or organization) | Identification No.) |

| 318 North Carson Street, Suite 208 |

| Carson City, NV 89701 USA |

| (Address of principal executive offices) |

Issuer’s telephone number, including area code: (949) 397-2522

Securities registered pursuant to Section 12(b) of the Act: None.

Securities registered pursuant to Section 12(g) of the Act: Common Stock, par value $0.0001 per share.

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No þ

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No þ

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes þ No ☐

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was Required to submit and post such files). þ Yes ☐ No

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. (as defined in Rule 12b-2 of the Exchange Act). Check one:

| Large accelerated filer | ☐ | Non-accelerated filer | ☐ |

| Accelerated Filer | ☐ | Smaller reporting company | þ |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No þ

As of June 30, 2014, the last day of the Registrant’s most recently completed second fiscal quarter, the aggregate market value of the registrant’s voting and none-voting common stock held by non-affiliates of the registrant was approximately: $2,974,514 at $0.08 per share, based on the closing price on the OTCQB.

As of March 31, 2015, there were outstanding 50,411,443 shares of the registrant’s common stock, $.0001 par value.

Documents incorporated by reference: None.

Next Graphite, Inc.

Form 10-K

Table of Contents

| Page | ||

| PART I | ||

| Item 1. | Business | 3 |

| Item 1A | Risk Factors | 16 |

| Item 2. | Properties | 21 |

| Item 3. | Legal Proceedings | 21 |

| Item 4. | Mine Safety Disclosures | 21 |

| PART II | ||

| Item 5. | Market for Registrant’s Common Equity and Related Stockholder Matters and Issuer Purchases of Equity Securities | 21 |

| Item 6. | Selected Financial Data | 24 |

| Item 7. | Management's Discussion and Analysis of Financial Condition and Results of Operations | 24 |

| Item 8. | Financial Statements and Supplementary Data | 25 |

| Item 9. | Changes in and Disagreements with Accountants on Accounting and Financial Disclosure | 25 |

| Item 9A | Controls and Procedures | 26 |

| Item 9B. | Other Information | 27 |

| PART III | ||

| Item 10. | Directors, Executive Officers and Corporate Governance | 28 |

| Item 11. | Executive Compensation | 30 |

| Item 12. | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | 32 |

| Item 13. | Certain Relationships and Related Transactions, and Director Independence | 32 |

| Item 14. | Principal Accountant Fees and Services | 33 |

| PART IV | ||

| Item 15. | Exhibits | 34 |

| Signatures | 35 | |

| Financial Statements | 36 | |

| 2 |

ITEM 1. BUSINESS

Corporate History

Next Graphite, Inc. (the “Company”) was incorporated under the name Zewar Jewellery, Inc. on September 26, 2012 in the State of Nevada. The business plan of the Company was originally to operate as an on-line imitation jewelry retailer. Immediately after the completion of the Share Exchange, the Company discontinued its on-line imitation jewelry business and changed its business plan to exploration and development of the license area covered by the License. Effective December 16, 2013, the Company changed its name to Next Graphite, Inc.

Share Exchange Agreement

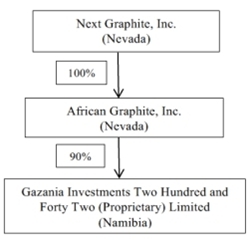

On November 14, 2013, we consummated transactions (the “Share Exchange”) pursuant to a Share Exchange Agreement (the “Share Exchange Agreement”) dated November 14, 2013 by and among the Company and the stockholders of African Graphite, Inc., a private Nevada corporation (“AGI” and the “AGI Stockholders”), whereby AGI Stockholders transferred 100% of the outstanding shares of common stock of AGI held by them, in exchange for an aggregate of 8,980,046 newly issued shares of the Company’s common stock, par value $.0001 per share (“Common Stock”).

Stock Purchase Option Agreement

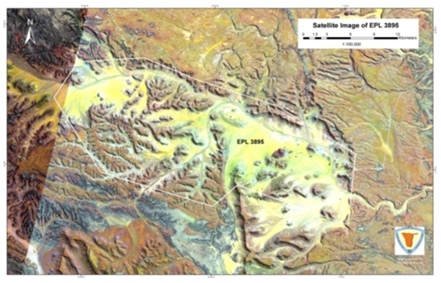

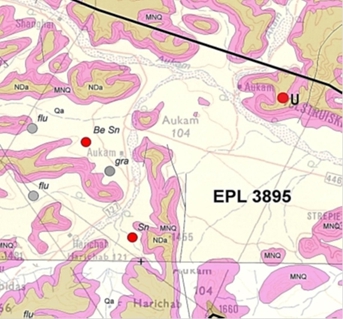

On November 14, 2013, AGI entered into a Stock Purchase Option Agreement (the “Option Agreement”) with NMC Corp., a corporation organized under the laws of the Province of Ontario, Canada (“NMC”), whereby NMC granted to AGI an option to purchase 90 ordinary shares, par value one Namibian dollar per share, of Gazania Investments Two Hundred and Forty Two (Proprietary) Limited, a corporation organized under the laws of the Republic of Namibia ("Gazania"), representing 90% of the issued and outstanding shares of Gazania, for $240,000. NMC had entered into an option agreement dated March 29, 2013, as amended on November 4, 2013 (the “Centre Agreement”), with Centre for Geoscience Research CC (formerly known as “Industrial Minerals and Rock Research Centre CC”), a company organized under the laws of the Republic of Namibia ("Centre"), whereby Centre agreed to transfer to Gazania 100% undivided interest in the exclusive prospecting license No. 3895 known as AUKAM originally issued to Centre by the government of the Republic of Namibia on April 4, 2011 and renewed on April 4, 2013 (the “License”). The License grants the right to conduct prospecting operations, bulk sampling and pilot production in the license area called AUKAM located in southern Namibia in the Karas Region within the Betaine district. The license area covers about 49,127 hectares. AUKAM is the only mine in Namibia which has produced graphite is situated in the license area. The ore body lies on the eastern slope of a prominent range of hills, which rises 120 to 150 meters above the level of the surrounding sand-covered valleys. The country rock consists almost entirely of grayish, medium-to-coarse grained granite and gneissic rocks of the Namaqualand Metamorphic Complex. The License applies to “base and rare metals” and “industrial minerals” and Gazania is the only party licensed to conduct mining operations of this type in the area. The transfer of the License to Gazania was approved by the Ministry of Mines and Energy of the Republic of Namibia on February 25, 2014.

Under the Option Agreement, AGI was required to pay to NMC $90,000 as an advance payment to be credited towards the purchase price of the Gazania shares. The Company made the advance payment on November 14, 2013. The balance of the purchase price in the amount of $150,000 was paid by AGI upon exercise of the Option that was completed on March 14, 2014. As a result, Gazania became a direct 90% owned subsidiary of AGI and an indirect subsidiary of the Company.

On November 14, 2013, the Company issued 12,600,003 shares of Common Stock to NMC in connection with the Option grant closing under the Option Agreement. In connection with the issuance of 12,600,003 shares of Common Stock, NMC entered into a Stock Escrow Agreement and a Lock-Up Agreement with the Company. Pursuant to the Stock Escrow Agreement, NMC delivered to the escrow agent the shares of Common Stock issued to it to be held by the escrow agent pending the closing of the Option exercise to purchase shares of Gazania by AGI under the Option Agreement in which case such 12,600,003 shares of Common Stock will be released by the escrow agent to NMC. The shares were released from escrow following the closing of the option exercise on March 14, 2013.

Under the Option Agreement, we undertook to provide at least $260,000 of working capital to or for the benefit of Gazania from the option grant closing date to June 30, 2014. The $260,000 of working capital was provided prior to June 30, 2014.

Under the Lockup Agreement executed on November 14, 2013, NMC agreed not to offer, pledge, sell, contract to sell, sell any option or contract to purchase, purchase any option or contract to sell, sell short, grant any option, right or warrant to purchase, lend or otherwise transfer or dispose of any shares of Common Stock, or enter into any swap or other arrangement that transfers any economic consequences of ownership of Common Stock until 12 months after the date therein.

| 3 |

Private Placement of Common Stock

From November 2013 to November 2014, the Company entered into and consummated transactions pursuant to a series of the Subscription Agreements (the “Subscription Agreements”) with certain accredited investors whereby the Company issued and sold to the investors for $1.00 per share an aggregate of 1,501,402 shares of the Company’s Common Stock for an aggregate purchase price of $1,501,400 (the “Private Placement”).

The Subscription Agreements contain representations and warranties by the Company and the investors which are customary for transactions of this type such as, with respect to the Company: organization, good standing and qualification to do business; capitalization; subsidiaries, authorization and enforceability of the transaction and transaction documents; valid issuance of stock, consents being obtained or not required to consummate the transaction; litigation; compliance with securities laws; and no brokers used, and with respect to the investors: authorization, accredited investor status and investment intent.

Stock Split

Effective December 16, 2013, a 7.8-for-1 forward stock split of the Company’s issued and outstanding Common Stock was effected (the “Stock Split”). As a result of the Stock Split, 9,602,569 shares of common stock issued and outstanding immediately before the Forward Split increased automatically, and without any further action from the Company’s stockholders, to 74,900,039 shares of common stock. The authorized number and par value of common stock were unchanged.

Consulting Agreement

On March 20, 2014, the Company entered into a consulting agreement with Wall Street Relations, Inc. (the “Consultant”). Under the agreement, the Consultant will provide to the Company public relations, communications, advisory and consulting services. The term of the agreement is 12 months. For the services to be rendered under the agreement, the Company paid to the Consultant an aggregate amount of $500,000 in cash.

On June 20, 2014, the Company terminated the agreement because of the Consultant’s failure to perform its obligations under the agreement. The Company is currently pursuing its options to obtain reimbursement of the fee paid to the Consultant under the agreement. As a result, the Company recorded a write off of prepaid assets of approximately $320,000 for the year ended December 31, 2014.

Private Placement of Secured Convertible Note

On October 2, 2014, the Company sold and issued to an accredited investor a secured convertible promissory note in the principal amount of $100,000 (the “2014 Note”), which is due and payable on December 31, 2015 and accrues interest at the rate of 5% per annum. In addition, all or any outstanding amount of the 2014 Note shall be convertible one year from the date of this Note at the Holder’s discretion into the Company’s stock at a 25% discount to the market price of the Company’s Common Stock at the time of conversion.

The foregoing descriptions of the 2014 Note are qualified in their entirety by reference to the provisions of the 2014 Note which is included as Exhibit 4.2 to this Report and is incorporated by reference herein.

Company’s Corporate Structure

Below is the Company’s current corporate structure:

| 4 |

Going concern

The Company's financial statements are prepared on a going concern basis, which contemplates the realization of assets and the satisfaction of obligations in the normal course of business. However, it has $17,878 in cash, has losses and an accumulated deficit, and a working capital deficiency. The Company does not currently have any revenue generating operations. These conditions, among others, raise substantial doubt about the ability of the Company to continue as a going concern.

In view of these matters, continuation as a going concern is dependent upon continued operations of the Company, which in turn is dependent upon the Company's ability to, meets its financial requirements, raise additional capital, and the success of its future operations. The financial statements do not include any adjustments to the amount and classification of assets and liabilities that may be necessary should the Company not continue as a going concern.

Management believes they can raise the appropriate funds needed to support their business plan and acquire an operating company with positive cash flow. Management intends to seek new capital from owners and related parties to provide needed funds.

Aukam Processing & Preliminary Economic Report

On February18, 2015, the Company’s lead geologist consultant Mr. Ian Flint prepared and issued a report that addresses building requirements for an overall processing circuit on site that would adequately accommodate the processing of Aukam graphite, initially targeted towards processing material from the on-site mine dumps. In August of 2014 Next carried out a 500 tonne bulk sampling program on the Aukam property, targeting the largest of three surface mine dumps. Through this sampling program it was discovered that the dumps contained a significant amount of graphitic lump material, which is easily separated from the mix. It was further recorded that a lump to waste ratio of 1:3 was averaged throughout the sample taken. From the 500 tonne sampling program 150 tonnes of lumps were separated out of the dumps by running the material over a screen specifically constructed for this purpose. The majority of the graphitic lumps ranged in purity from 40-80% graphite with an average grade of 42%, and a residual 350 tonnes of lesser grade material graded an average of 34% graphite. In December of 2014, the Company reported additional testing from Gecko Laboratories, Namibia, including industry–standard flotation tests that reported the flotation characteristics of its lump graphite that influenced the Company’s plant design. The tests were conducted on 1,763 pounds of composite samples drawn from the 150 tonnes of pre-screened graphitic lump, residual and waste material. Flotation tests carried out on samples and then tested for purity and grade demonstrated a 212-micron grind was the optimal size for flotation, and delivered a result of 97.1 % pure graphite after a single, rougher float. An average of 96.2 % graphite was recorded in the concentrates across all samples including waste material.

Below is a brief summary of Mr. Ian Flint’s biographical information:

Mr. Ian Flint holds a PhD in Mining and Mineral Processing Engineering from the University of British Columbia, and a Master of Science degree in Metallurgical Engineering and Bachelor of Science degree in Geological Engineering, both from the University of Toronto. He has 24 years of graphite experience, including geology, test work, pilot plants, circuit design, mine development, purchasing, management, marketing and service as a public company corporate director. Mr. Flint is currently on a project for Elcora Resources Corp. (TSXV: ERA), and he has previously worked on projects for companies such as the Graphene Corporation, Dalhousie, Integrated Carbonics, Quinto, Bissett Creek, Mount Cameron Minerals, Worldwide Graphite (Superior), Farrell, Crystal Graphite, Victoria Graphite, CalGraphite. He worked as a technical advisor to Innovacorp during June 2011 through August 2013 and he served as Vice President at Champlain Tidal Energy Corp. Ltd. between 2009 and 2010. Mr. Flint has served on the Board or Advisor to several mining and graphite companies including, The Graphene Corporation, Dalhousie, Integrated Carbonics, Quinto, Bissett Creek, Mount Cameron Minerals, Worldwide Graphite (Superior), Farrell, Crystal Graphite, Victoria Graphite, CalGraphite.

New Potential Business Relationships

The Company is in discussions with off takers for the purchase, initially, of high grade unprocessed graphite from its existing 140,000 tonnes of tailing heaps. It is also in discussions with a firm relative to a joint venture arrangement that would begin in the second quarter of 2015 and would include the funding and installation of a processing facility at the Company’s Aukam mine site.

Our Business

Next Graphite, Inc. is an exploration/development stage company targeting the growing global graphite production industry with the Company's 125,000-acre Africa-based Aukam Graphite Project. The Aukam Graphite Mine was established in 1940 in the current Republic of Namibia, produced USD $30 million of graphite at today's prices. The Graphite property is estimated to still contain a significant amount of high grade, vein type graphitic material. Global graphite demand is being driven by the development of new markets for clean and efficient energy alternatives, smart grid infrastructure and military capabilities. Next Graphite has an immediately available, surface-visible, estimated 140,000-tonne mine heaps along with competitive projected mining and processing costs. The completion of GPNE's Aukam Graphite Mine re-launch and development activities are expected to result in a multi-million dollar inward investment into Namibia commencing in 2015.

Global graphite demand is being driven by the development of new markets for clean and efficient energy alternatives, smart grid infrastructure and military capabilities.

| 5 |

Location of the Project and Infrastructure

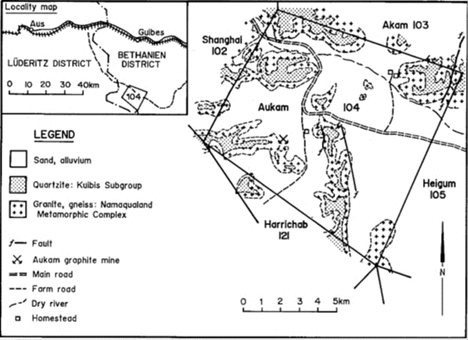

The Aukam Graphite Mine is located in southern Namibia in the Karas region within the Betanie district 169 km from the port of Luderitz. The nearest town of Aus is some 87 km away by road. The license area spurns about 49,127 hectares stratiform base metal that form part of the Namaqualand meta-sedimentary sequence.

The infrastructure in the area is good with access to the site possible throughout the year. The Aukam Graphite deposit is relatively close to a main tar road and well graded so the only construction required would be an approximately 2 km long access road to the site. There is a national power grid that passes right by the property. Water is available in large amounts from underground aquifers. The nearest rail link is located next to the main highway (some 70 km from the site).

Climate

The Aukam Graphite Mine deposit is located in an unusual area of southern Namibia with both summer and winter rainfall. In the austral summer, day-time temperature peak in the mid 40° Celsius, while in winter temperatures can go as low as freezing. Rainfall in winter is generally light drizzle with occasional harder falls and sometimes flurries. In summer, the rainfall is associated with occasional thunderstorms and is of short duration, but can be of very high intensity. All of the streams within the area are ephemeral and can flow very strongly after summer rainfall. Average annual rainfall is 50-150 mm.

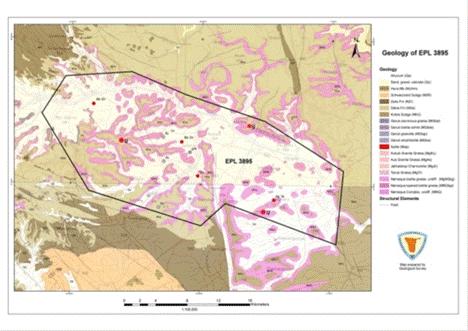

Geology

The Aukam Graphite Mine is the only mine in Namibia which has produced graphite. The ore body lies on the eastern slope of a prominent range of hills which rises 120 to 150 meters above the level of the surrounding sand covered valleys. The country rock consists almost entirely of grayish, medium- to coarse grained granite and gneissic rocks of the Namaqualand Metamorphic Complex.

| 6 |

The graphite-bearing zone, which strikes east-west, is about 10 m wide and is traceable over a distance of some 350 m. The graphite, which is of the fine-flaky to lumpy type, usually contains malachite specks, while sulphur occurs along cracks. The graphite veins are flanked by a pale green, highly epidotized and kaolinized granite which is soft and highly decomposed. Parallel stringers of ferruginous and micaceous talcose material are associated with the veins.

| 7 |

Graphite deposit in the Aukam Graphite Mine

The best quality graphite is located in the central lode and was initially worked by opencast mining along the slope, as the softness of the rocks in this area greatly facilitated mining operations. The excavation, which now measures 45 by 35 m, was later supplemented by two adits sited further downhill along the same lode, and a third was developed above the opencast pit. The lowermost tunnel is about 120 m long. Large-scale sloping from these adits yielded several thousand tons of graphite. The deposit was mined from 1940 to 1956 when the workings were destroyed by fire. Production was resumed in 1964 and ceased in 1974.

| 8 |

Graphite occurs as veins and lenses in the East-West striking vertical zone, 10m wide and 350m long. At the bottom of the hill it disappears underneath the sand cover, whereas near the summit it peters out. The zone comprises three parallel lodes. Veins, lenses and pockets of ore, several meters wide, dip 70o to 90o to the south.

Graphite and its Industrial Uses

Graphite is considered to be the purest form of carbon. Graphite is an excellent conductor of heat and electricity and has a high melting temperature of 3,500 degrees Celsius. It is extremely resistant to acid, chemically inert and highly refractory. The utility of graphite is dependent largely upon its type.

There are three principal types of natural graphite, each occurring in different types of ore deposits:

| ● | Crystalline flake graphite, or flake graphite, occurs as isolated, flat, plate-like particles with hexagonal edges, if unbroken, and when broken, the edges can be irregular or angular. | |

| ● | Amorphous graphite occurs as fine particles and is the result of thermal metamorphism of coal, the last stage of coalification, and is sometimes called meta-anthracite. Very fine flake graphite is sometimes called amorphous in the trade. | |

| ● | Lump graphite, or vein graphite, occurs in fissure veins or fractures and appears as massive platy intergrowths of fibrous or acicular crystalline aggregates, and is probably hydrothermal in origin. |

All grades of graphite, especially high grade amorphous and crystalline graphite that remains suspended in oil are used as lubricants. Graphite has an extraordinarily low co-efficient of friction under most working conditions. This property is invaluable in lubricants. It diminishes friction and tends to keep the moving surface cool. Dry graphite as well as graphite mixed with grease and oil is utilized as a lubricant for heavy and light bearings. Graphite grease is used as a heavy-duty lubricant where high temperatures may tend to remove the grease.

The flake type graphite is found to possess extremely low resistivity to electrical conductance. The electrical resistivity decreases with the increase of flaky particles. The bulk density decreases progressively as the particles become flakier. Because of this property in flake graphite, it is used in the manufacture of carbon electrodes, plates and brushes required in the electrical industry and dry cell batteries. Flake graphite has been replaced to some extent by synthetic, amorphous, crystalline graphite and acetylene black in the manufacture of plates and brushes. Flake graphite containing 80 to 85% carbon is used for crucible manufacture; graphite containing a carbon content of 93% and above is preferred for the manufacture of lubricants, and graphite containing a carbon content of 40 to 70% is utilized for foundry facings. Natural graphite, refined or otherwise pure, having carbon content not less than 95% is used in the manufacture of carbon rods for dry battery cells.

The Industry

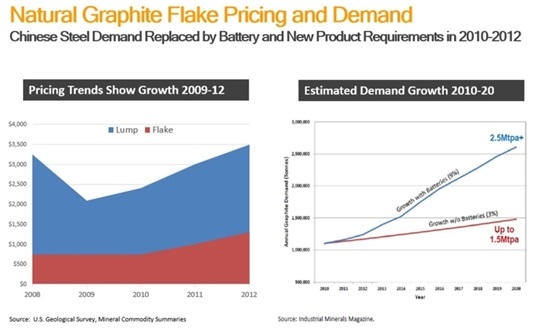

The recent surge in interest and value of graphite is built on long-standing and solid fundamentals as a well-established industrial mineral. Natural graphite has been mostly consumed in steel making; for refractories and foundry facings; as a lubricant and as a containment lining in nuclear applications. Other uses have included automobile brake linings and transmission components, but with the extraordinary increase in the use of lithium-Ion batteries, graphite has experienced a huge growth surge and the auto industry is sure to be at the forefront of this growth.

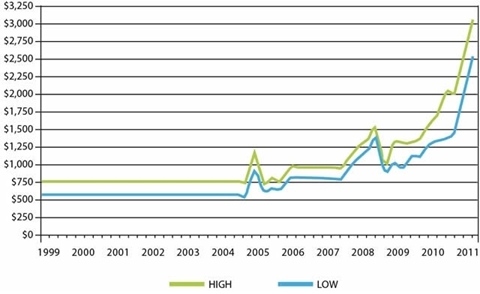

Prices of large-flake, high carbon graphite has increased from $600 per metric ton during the 1990s to highs of approximately $2,500 per metric ton recently. Industry participants believe that positive trends in graphite prices could continue in the coming years as China is expected to continue to tighten regulations regarding exports of graphite.

The statements made in this section, “The Industry,” reflect management opinions and beliefs based on the information obtained from a variety of sector and industry sources. These include but are not limited to: Angel Publishing, Industrial Minerals Magazine, RR Market Research, and the U.S. Geological Survey of Mineral Commodity Summaries.

| 9 |

A report by Industrial Minerals, a leading source of information on critical minerals, stated that the Chinese government is focused on consolidating the domestic graphite industry and is going ahead with plans to reduce the number of graphite mines in Hunan province from 230 to around 20, with increased government supervision aimed at reducing environmental impact due to harmful mining practices. This is expected to lead to a loss of around 100,000 metric tons of graphite per year, or approximately 10 percent of the global supply.

Recent prices for flake graphite have seen $1,500 - $3,000 per tons depending on flake size and grade. Graphite prices have seen increases for large flake, high purity graphite (+80 mesh, 94-97%C) and have more than doubled in recent years. China, which produces about 80 percent of the world's graphite, is reducing its 200 amorphous graphite mines to 20 and creating a state-run monopoly causing disruptions in supply. Industrial Minerals recently reported exports from China in January and February 2012 have been reduced by 55.3% and 60.1% from 2011 level exports from Hunan Province. It is not expected that current graphite mines in other countries could replace Chinese amorphous supply.

| 10 |

World demand to rise 6% annually through 2018

Worldwide demand for natural and synthetic graphite (including carbon fiber) is forecast to expand six percent per annum to about 3.9 million metric tons in 2018. This is an improvement over the 2008-2013 pace. Three key trends are expected to fuel this growth. First, advances in manufactured goods are expected to spur graphite consumption. Second, steelmaking and other types of metallurgy activity, important markets for graphite, are expected to accelerate between 2013 and 2018. Third, the global graphite market will benefit greatly from the rise of new, technologically advanced applications, including graphene, pebble-bed nuclear reactors, fuel cells, solar power, and aerospace. [Source: RR Market Research World Graphite (Natural, Synthetic & Carbon Fiber to 2018)]

Natural flake graphite to outpace amorphous types

In the natural graphite segment flake graphite is anticipated to capture market share from amorphous graphite as high tech applications become more important and the availability of flake graphite increases. Through 2018, worldwide demand for flake graphite is expected to grow more than twice as fast as for amorphous products. When China reduced natural graphite output between 2011 and 2013 because of environment and industry fragmentation concerns, a large number of exploration projects were launched around the world. Approximately 30 companies are now working on developing mines in countries such as Australia, Canada, Russia, South Korea, Sweden, and the US. Finally, interest in natural graphite has increased dramatically with the rise of lithium ion batteries, which are used in electronics and electric motor vehicles.

The synthetic graphite market is also likely to see healthy gains during the 2013-2018 period. Worldwide demand for carbon fiber is expected to grow at a double-digit annual pace through 2018, as its use in aerospace, automotive, wind turbine, and other applications increases sharply. Additionally, the cost of carbon fiber is expected to gradually decline between 2013 and 2018 because of technological innovation. The growing use of electric arc furnaces to produce steel in most parts of the world is expected to boost sales of graphite electrodes. As synthetic graphite becomes more widely available in industrializing countries, product demand will grow. However, increasing production capacity will moderate prices. [Source: RR Market Research World Graphite (Natural, Synthetic & Carbon Fiber to 2018, online research)]

China to remain key market

Roughly 45 percent of all additional graphite demand generated between 2013 and 2018 is expected to be attributable to China, also the world’s leading consumer of these products. Growth will be bolstered by gains in manufactured goods shipments, increases in metallurgy activity, and additional investment in technologically advanced industries. Other industrializing countries in the Asia/Pacific region are also expected to perform well between 2013 and 2018, as their manufacturing sectors expand and grow in sophistication. Additionally, the availability of graphite products in Asia/ Pacific countries is anticipated to increase.

| 11 |

Graphite consumption in North America is forecast to expand by nearly six percent per annum between 2013 and 2018. This is a significant improvement over the 2008-2013 pace. The US is expected to register the region’s fastest growth, as industrial production increases, metallurgy activity rebounds, and lithium ion battery output surges. Led by Brazil, Central and South America is projected to see sales of graphite increase at the second fastest annual rate worldwide through 2018. [Source: RR Market Research World Graphite (Natural, Synthetic & Carbon Fiber to 2018, online research)]

Graphite’s new era of demand

Natural graphite appears to be entering a new era of demand. Faced by a perfect storm of factors the world’s graphite supply is in uncertain times. Graphite’s diversity has secured a strong suite of traditional end use markets over the last 100 years as refractories, metallurgy, lubricants, carbon products such as car brake pads and pencils, and many other products, have carved out a substantial business for many producers around the world. However, it is the emergence of the Li-ion battery era that has the potential to turn the industry on its head. Portable electronic devices: mobile phones, iPads, and power tools, and large scale energy storage, all favor Li-ion technology. It is anticipated that electric vehicles hold the potential demand clout that could revolutionize the graphite space. The potential for graphite does not stop there. The wild card is the new super-material graphene. Derived from a single layer of graphite, graphene is over 100 times stronger than steel and more conductive than copper while being incredibly light. The applications of graphene seem to be endless, but it is yet to be commercialized. Very soon, the industry may not have enough natural graphite to go around. [Source: The Natural Graphite Report, 2012.]

China

The world is currently at the mercy of Chinese supply, which accounted for 79% of the world’s natural graphite in 2011. China’s graphite production power was on display twenty years ago when huge volumes of new supply came into the world market rendering smaller mines in Canada, Mexico, Europe, and Australia uneconomic. Now China has focused on serving its own domestic needs and the manufacture of higher value goods. China’s desire to build a value-chain means it no longer wants to be the source of raw materials, but the source of processed and finished products.

This situation holds the potential to be a graphite game-changer. A generation of under investment in mines around the world is now being felt. However, exploration is underway, particularly in Canada and Brazil, and new mines are under development. Some of the questions facing the industry are the following:

| ● | How long will this new supply take to come to fruition? | |

| ● | Will the quality and volumes be sufficient? | |

| ● | Is there room for more players? | |

| ● | Are there already too many producers? |

Prices up 140%

A supply/demand situation has been simmering for the last five years. Since 2010 the price of high quality flake grades of natural graphite have increased by 140% as a result of Chinese policy and struggling production elsewhere. The price pattern is recurring: that of a stabilization followed by an increase. One thing seems certain –that graphite is not losing its value. The talk in, and outside of, the industry is on what the future will hold for natural graphite. The rate of exploration in the second half of 2011 has levels not seen in a generation and Canada is leading the way on new projects. The unknowns that are electric vehicles and large scale energy storage together with China at a rapid stage of economic development, leaves the future for the key raw material uncertain.

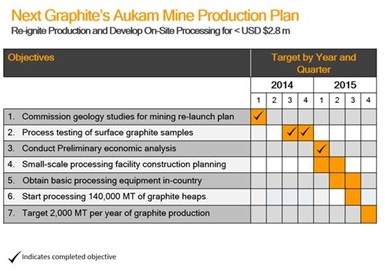

Our Strategy

The Company has prepared a plan to re-launch mining production and on-site processing at an estimated cost, from inception, of $2,750,000. The completed, re-opened mine will initially be targeting an estimated 5,000 tons of annual production.

In 2014, we conducted the following pre-production activities: the transfer of the mining license to Next Graphite Inc.; initial testing of the Aukam Graphite Mine samples and the compilation of its initial geological report; process testing of surface graphite samples from on-site tailings; preparation of an Environmental Impact Assessment report; application for a Mining License for extraction; preliminary drilling and advanced product testing; preliminary economic analysis based on our findings and a scoping study that details the engineering for production, mining design, flowchart and operations; construction planning for a small-scale processing facility; and continuing public company governance, overhead & professional services.

In 2015, the Company plans to build an on-site processing plant and begin processing its existing 140,000 tons of graphite tailings. The Company is targeting to initially reach graphite production of up to 2,000 tons per year commencing in the second half of 2015. The approximately 140,000 tonnes of mine heaps currently sitting at the surface is a legacy of the former mining operations on site. The pile still contains a large concentration of graphitic material. Through a recent bulk testing program conducted in June-August 2014, the Company was able to recover 137 metric tonnes of graphite lumps from 455 metric tonnes of material passed through a separation screen. The average lump-to-waste ratio in the piles with an average of ±70 recovery was 1:3. If these results continue the Company can expect that approximately 30,000 tonnes of graphitic lumps will still be present in the heaps. The former average grade per lump was about 42% carbon. This indicates that within the piles alone there could be as much as 15,000 tonnes of graphite. 80 samples were submitted to a laboratory in Namibia for testing to determine the average grade of the recovered lumps. The results as reported in December 2014 were positive. Historically 300,000 tonnes of material was mined from the Aukam site, from which 25,000 tonnes of graphite was recovered.

| 12 |

Historically 300,000 tonnes of material was mined from the Aukam site, from which 25,000 tonnes of graphite was recovered.

The Company intends to capitalize upon the increasing worldwide demand for high-grade graphite in a cost-effective and potentially profitable fashion, overseen by a highly experienced management team:

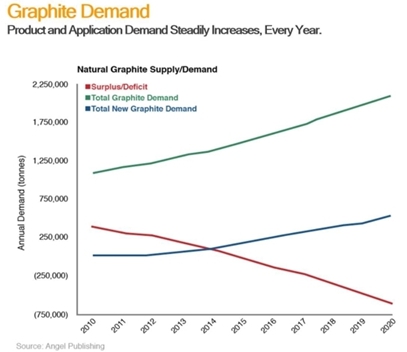

| ا§ | The Global Graphite market, currently estimated at $12 billion, is expected to grow at a Compound Aggregate Growth Rate (“CAGR”) of 5.5% during 2012-2016. One key factor is the increasing use of graphite in batteries, e.g., the Li-Ion market is estimated at ~$250B by 2020 [Source: ReportStack, “Global Graphite Market 2012-2016”]. | |

| ا§ | Next Graphite has secured the mining rights to a mine with proven resources that has already been historically operated (has previously produced USD $30 million of graphite at today’s prices, and is estimated by the Company’s geological consultants to contain over 4 million tons of natural, high-grade, large-flake, hydrothermal-sourced graphite reserves) | |

| ا§ | The Company plans to be operating in the Republic of Namibia, a country that is mining-friendly, has infrastructure in place, and has low labor costs. |

Market, Customers and Distribution Methods

Although there can be no assurance, large and well capitalized markets are readily available for all metals and precious metals throughout the world. A very sophisticated futures market for the pricing and delivery of future production also exists. The price for metals is affected by a number of global factors, including economic strength and resultant demand for metals for production, fluctuating supplies, mining activities and production by others in the industry, and new and or reduced uses for subject metals.

The mining industry is highly speculative and of a very high risk nature. As such, mining activities involve a high degree of risk, which even a combination of experience, knowledge and careful evaluation may not be able to overcome. Few mining projects actually become operating mines. The mining industry is subject to a number of factors, including intense industry competition, high susceptibility to economic conditions (such as the price of metal, foreign currency exchange rates, and capital and operating costs), and political conditions (which could affect such things as import and export regulations, foreign ownership restrictions). Furthermore, the mining activities are subject to all hazards incidental to mineral exploration, development and production, as well as risk of damage from earthquakes, any of which could result in work stoppages, damage to or loss of property and equipment and possible environmental damage. Hazards such as unusual or unexpected geological formations and other conditions are also involved in mineral exploration and development.

Our methods of distributing our mined graphite will in part be dictated by what our initial drilling activities indicate relative to quality, quantity, concentration and cost of extraction.

The options we are considering include:

| ● | marketing department that sells the Company’s graphite to end users. This will probably not be pursued unless we are mining at least 5,000 - 10,000 tonnes of graphite a year. | |

| ● | market the graphite through a partnership with another graphite mine. | |

| ● | market the material, via offtakes, to graphite distributors, traders or other companies that may market graphite from more than one mining company. |

| 13 |

The Company’s costs of operation will also be largely influenced by the factors noted above such as quality, quantity, concentration, and cost of extraction. Based on our initial planned small-scale operation, the cost to build our processing plant will be approximately $1,000,000. We anticipate our on-going costs of operation will be relatively low given our low Namibian labor costs and low extraction costs based on preliminary testing.

Intellectual Property

The Company does not have any Intellectual Property at this time.

Competition

The mineral exploration industry is highly competitive. We are a new exploration stage company and have a weak competitive position in the industry. We compete with junior and senior mineral exploration companies, independent producers and institutional and individual investors who are actively seeking to acquire mineral exploration properties throughout the world together with the equipment, labor and materials required to operate on those properties. Competition for the acquisition of mineral exploration interests is intense with many mineral exploration leases or claims available in a competitive bidding process in which we may lack the technological information or expertise available to other bidders.

Many of the mineral exploration companies with which we compete for financing and for the acquisition of mineral exploration properties have greater financial and technical resources than those available to us. Accordingly, these competitors may be able to spend greater amounts on acquiring mineral exploration interests of merit or on exploring or developing their mineral exploration properties. This advantage could enable our competitors to acquire mineral exploration properties of greater quality and interest to prospective investors who may choose to finance their additional exploration and development. Such competition could adversely impact our ability to attain the financing necessary for us to acquire further mineral exploration interests or explore and develop our current or future mineral exploration properties.

We also compete with other junior mineral exploration companies for financing from a limited number of investors that are prepared to invest in such companies. The presence of competing junior mineral exploration companies may impact our ability to raise additional capital in order to fund our acquisition or exploration programs if investors perceive that investments in our competitors are more attractive based on the merit of their mineral exploration properties or the price of the investment opportunity. In addition, we compete with both junior and senior mineral exploration companies for available resources, including, but not limited to, professional geologists, land specialists, engineers, camp staff, helicopters, float planes, mineral exploration supplies and drill rigs.

General competitive conditions may be substantially affected by various forms of energy legislation and/or regulation introduced from time to time by the governments of the United States and other countries, as well as factors beyond our control, including international political conditions, overall levels of supply and demand for mineral exploration. In the face of competition, we may not be successful in acquiring, exploring or developing profitable mineral properties or interests, and we cannot give any assurance that suitable oil and gas properties or interests will be available for our acquisition, exploration or development. Despite this, we hope to compete successfully in the mineral exploration industry by:

| ● | keeping our costs low; | |

| ● | relying on the strength of our management’s contacts; and | |

| ● | using our size and experience to our advantage by adapting quickly to changing market conditions or responding swiftly to potential opportunities. |

Government Regulation

In Namibia, all mineral rights are vested in the state. The Minerals (Prospecting and Mining) Act of 1992 regulates the mining industry in the country. The Ministry of Mines and Energy is responsible for mining. Licenses and permits are authorized by the Minister on recommendation of the Mining Commissioner. Namibia's mining industry is also regulated by the Minerals Development Fund of Namibia Act of 1996 and the Diamond Act of 1999. Several types of mining and prospecting licenses exist as follows:

| ● | Non-Exclusive Prospecting Licenses, valid for 12 months, permit prospecting non-exclusively in any open group not restricted by other mineral rights. | |

| ● | Reconnaissance Licenses allow regional remote sensing techniques, and are valid for 6 months (renewable under special circumstances) and can be made exclusive in some instances. | |

| ● | Exclusive Prospecting Licenses can cover areas not exceeding 1000 square kilometers and are valid for 3 years, with two renewals of 2 years each and discretionary renewals thereafter. Two or more EPLs can be issued for more than one mineral in the same area. | |

| ● | Mineral Deposit Retention Licenses (MDRLs) allow successful prospectors to retain rights to mineral deposits which are uneconomical to exploit immediately. MDRLs are valid for up to 5 years and can be renewed subject to limited work and expenditure obligations. | |

| ● | Mining Licenses can be awarded to Namibian citizens and companies registered in Namibia. They are valid for an initial 25 years, renewable up to 15 years at a time. | |

| ● | There is no requirement that the Government should hold equity participation in mining ventures. |

We will be required to comply with the foregoing government regulations. An Environmental Impact Analysis was prepared and accepted by the Namibia Ministry of Environment and Tourism on September 22, 2014. We have submitted an extension to our current Exploratory License and are confident of it being renewed.

| 14 |

Additional approvals and authorizations may be required from other government agencies, depending upon the nature and scope of the proposed exploration program. The amount of these costs is not known as we do not know the size, quality of any resource or reserve at this time. It is impossible to assess the impact of any capital expenditures on earnings or our competitive position.

Environmental Regulations

Our exploration activities are also subject to laws and regulations of Namibia governing protection of the environment. These laws are continually changing and, as a general matter, are becoming more restrictive. Our policy is to conduct business in a way that safeguards public health and the environment and in material compliance with applicable environmental laws and regulations. Changes to current laws and regulations in the jurisdictions where we operate could require additional capital expenditures and increased operating costs. Although we are unable to predict what additional legislation and the associated costs of such legislation, if any, might be proposed or enacted, additional regulatory requirements could render certain exploration activities uneconomic.

Employees

As of December 31, 2014, the Company and its subsidiaries had no employees. The Company utilizes the services of consultants and advisors. These include its principal executive officer, chief financial officer, geological personnel, accountants, and attorneys. Some of these positions, especially those of a technical nature, may be converted to employment if and when the Company's business requires and resources permit.

Emerging Growth Company

The Company is an “emerging growth company”, as defined in the Jumpstart Our Business Startups Act of 2012 (“JOBS Act”), and may take advantage of certain exemptions from various reporting requirements that are applicable to other public companies that are not “emerging growth companies” including, but not limited to, not being required to comply with the auditor attestation requirements of section 404(b) of the Sarbanes-Oxley Act, and exemptions from the requirements of Sections 14A(a) and (b) of the Securities Exchange Act of 1934 to hold a nonbinding advisory vote of shareholders on executive compensation and any golden parachute payments not previously approved.

The Company has elected to use the extended transition period for complying with new or revised accounting standards under Section 102(b)(1) of the JOBS Act. This election allows us to delay the adoption of new or revised accounting standards that have different effective dates for public and private companies until those standards apply to private companies. As a result of this election, our financial statements may not be comparable to companies that comply with public company effective dates.

We will remain an “emerging growth company” until the earliest of (1) the last day of the fiscal year during which our revenues exceed $1 billion, (2) the date on which we issue more than $1 billion in non-convertible debt in a three year period, (3) the last day of the fiscal year following the fifth anniversary of the date of the first sale of our common equity securities pursuant to an effective registration statement filed pursuant to the Securities Act of 1933, as amended, or (4) when the market value of our common stock that is held by non-affiliates exceeds $700 million as of the last business day of our most recently completed second fiscal quarter.

To the extent that we continue to qualify as a “smaller reporting company”, as such term is defined in Rule 12b-2 under the Securities Exchange Act of 1934, after we cease to qualify as an emerging growth company, certain of the exemptions available to us as an emerging growth company may continue to be available to us as a smaller reporting company, including: (1) not being required to comply with the auditor attestation requirements of Section 404(b) of the Sarbanes Oxley Act; (2) scaled executive compensation disclosures; and (3) the requirement to provide only two years of audited financial statements, instead of three years.

| 15 |

ITEM 1A. RISK FACTORS

An investment in the Company is subject to risks and uncertainties. The occurrence of any one or more of these risks or uncertainties could have a material adverse effect on the value of any investment in the Company and the business, prospects, financial position, financial condition or operating results of the Company. Prospective investors should carefully consider the information presented in this report, including the following risk factors, which are not an exhaustive list of all risk factors associated with an investment in the Company or the Company’s shares or in connection with the operations of the Company:

The Company has a limited history of operations and Aukam Graphite Project is the Company’s sole asset. There can be no assurance that any of the Company’s planned exploration and development activities on the Aukam Graphite Project will ever lead to the re-launch of graphite production from it.

The Company has a limited history of operations and is in the early stage of development. The Company is engaged in the business of exploring, resuming production and developing a single asset, the Aukam Graphite Project, in the hope of ultimately, at some future point, placing the Aukam Graphite Project back into production. The Aukam Graphite Project will be for the foreseeable future the Company’s sole asset. Although management believes the Aukam Graphite Project has sufficient merit to justify focusing all the Company’s limited resources upon it, the Company will in consequence be exposed to some heightened degree of risk due to the lack of property diversification. The Aukam Graphite Project is assumed to still host graphitic material that has been historically mined. However, there are no guarantees that the re-launched production of these potentially indicated and inferred resources will ever be demonstrated, in whole or in part, to be profitable to mine. Development of the Aukam Graphite Project will only follow upon obtaining satisfactory results from the recommended multi-phase testing, exploration and development program and any subsequent work and studies that may be required. There can be no assurance that any of the Company’s planned exploration and development activities on the Aukam Graphite Project will ever lead to the re-launch of graphite production from it.

There is no guarantee that the mineral deposit contained in the Aukam Graphite Project will be commercially viable.

The exploration and development of mineral projects is highly speculative in nature and involves a high degree of financial and other risks over a significant period of time, which even a combination of careful evaluation, experience and knowledge may not reduce or eliminate. The Aukam Graphite Project will constitute the Company’s sole asset. However, there are no guarantees that there will ever be a profitable mining operation on the Aukam Graphite Project. The proposed multi-phase exploration and development program on the Aukam Graphite Project is subject to a significant degree of risk. Whether a mineral deposit will be commercially viable depends on a number of factors, including the particular attributes of the deposit (i.e. size, grade, access, flake size distribution, contaminants, and proximity to infrastructure), financing costs, the cyclical nature of commodity prices and government regulations (including those relating to prices, taxes, currency controls, royalties (both product and monetary), land tenure, land use, importing and exporting of mineral products, and environmental protection). The effect of these factors or a combination thereof cannot be accurately predicted but could have an adverse impact on the Company.

The Company has no history of mineral production.

Even though the Aukam Graphite Project has produced graphite historically, the Company has never had an interest in a mineral-producing property. There is no assurance that commercial quantities of minerals will be discovered at any future properties, nor is there any assurance that any future exploration programs of the Company on the Aukam Graphite Project or any future properties will yield any positive results. Even where commercial properties of minerals are discovered, there can be no assurance that any property of the Company will ever be brought to a stage where mineral reserves can be profitably produced thereon. Factors that may limit the ability of the Company to produce mineral resources from its property include, but are not limited to, the price of mineral resources are explored, availability of additional capital and financing and the nature of any mineral deposits.

The Company’s operations will be subject to all of the hazards and risks normally encountered in mineral exploration and development. The Company does not currently carry insurance against these risks and there is no assurance that such insurance will be available in the future, or if available, at economically feasible premiums or acceptable terms.

Mining operations generally involve a high degree of risk. The Company’s operations will be subject to all of the hazards and risks normally encountered in mineral exploration and development. Such risks include unusual and unexpected geological formations, seismic activity, rock bursts, cave-ins, water inflows, fires and other conditions involved in the drilling and removal of material, environmental hazards, industrial accidents, periodic interruptions due to adverse weather conditions, labor disputes, political unrest and theft. The occurrence of any of the foregoing could result in damage to, or destruction of, mineral properties or interests, production facilities, personal injury, damage to life or property, environmental damage, delays or interruption of operations, increases in costs, monetary losses, legal liability and adverse government action. The Company does not currently carry insurance against these risks and there is no assurance that such insurance will be available in the future, or if available, at economically feasible premiums or acceptable terms. The potential costs associated with losses or liabilities not covered by insurance coverage may have a material adverse effect upon the Company’s financial condition.

| 16 |

The Company has a limited operating history and financial resources.

The Company has a limited operating history, has no operating revenues and is unlikely to generate any revenues from operations in the immediate future. Its existing cash resources are not sufficient to cover its projected funding requirements for the ensuing year. If its phased exploration and development program is successful, additional funds will be required to bring the Aukam Graphite Project back into production. The Company has limited financial resources and there is no assurance that sufficient additional funding will be available to enable it to fulfill its obligations or for further exploration and development on acceptable terms or at all. Failure to obtain additional funding on a timely basis could result in delay or indefinite postponement of further exploration and development and could cause the Company to reduce or terminate its operations.

If we cease to continue as a going concern, due to lack of funding or otherwise, you may lose your entire investment in the Company.

Our current plans indicate that we will need substantial additional capital to implement our plan of operations before we have any anticipated revenues. When we require additional funds, general market conditions or the then-current market price of our common stock may not support capital raising transactions such as additional public or private offerings of our common stock. If we require additional funds and we are unable to obtain them on a timely basis or on terms favorable to us, we may be required to scale back our development of new products, sell or license some or all of our technology or assets, or curtail or cease operations.

The Company is subject to Namibian government regulation of its mining operations. Although the Company believes that the Aukam Graphite Project is in substantial compliance with all material laws and regulations that currently apply to its activities, there can be no assurance, however, that the Company will obtain on reasonable terms or at all the permits and approvals, and the renewals thereof, which it may require for the conduct of its future operations or that compliance with applicable laws, regulations, permits and approvals will not have an adverse effect on plans to explore and develop the Aukam Graphite Project.

The future operations of the Company, including exploration and development activities and the commencement and continuation of commercial production, require licenses, permits or other approvals from various federal, provincial and local governmental authorities and such operations are or will be governed by laws and regulations relating to prospecting, development, mining, production, exports, taxes, labor standards, occupational health and safety, waste disposal, toxic substances, land use, water use, environmental protection, land claims of indigenous people and other matters. The Company believes that the Aukam Graphite Project is in substantial compliance with all material laws and regulations that currently apply to its activities. There can be no assurance, however, that the Company will obtain on reasonable terms or at all the permits and approvals, and the renewals thereof, which it may require for the conduct of its future operations or that compliance with applicable laws, regulations, permits and approvals will not have an adverse effect on plans to explore and develop the Aukam Graphite Project. Possible future environmental and mineral tax legislation, regulations and actions could cause additional expense, capital expenditures, restrictions and delay on the Company’s planned exploration and operations, the extent of which cannot be predicted.

Failure to comply with applicable laws, regulations and permitting requirements may result in enforcement actions thereunder, including orders issued by regulatory or judicial authorities causing operations to cease or be curtailed, and may include corrective measures requiring capital expenditures, installation of additional equipment, or remedial actions. Parties engaged in mining operations may be required to compensate those suffering loss or damage by reason of the mining activities and may have civil or criminal fines or penalties imposed for violations of applicable laws or regulations.

The initial property report was based on production data generated from the Namibian Ministry of Mines and Energy and from prior exploration work. There is no guarantee in reliability of such data.

In preparing the initial property report, The Aukam Property Geological Report of February 16, 2014, the authors of that report from Element 12 Consulting relied upon certain data generated on production from the government-mining ministry, and by exploration work carried out by geologists employed by others. There is no guarantee that data generated from government records or by prior exploration work is 100% reliable and discrepancies in such data not discovered by the Company may exist. Such errors and/or discrepancies, if they exist, could have impact on the accuracy of the subject report.

| 17 |

If we lose the services of key management personnel and are unable to attract and retain highly skilled employees, we may not be able to execute our business strategy effectively.

The success of the Company will be largely dependent upon the performance of its senior management and directors. Due to the relative small size of the Company, the loss of these persons or the inability of the Company to attract and retain additional highly skilled employees may adversely affect its business and future operations. The Company has not purchased any “key-man” insurance nor has it entered into any non-competition or non-disclosure agreements with any of its directors, officers or key employees and has no current plans to do so.

While our executive officers and directors are highly experienced in business, they do not come from the mining industry and rely on Company managers and consultants for specific mining expertise. The Company has hired and may continue to rely upon consultants and others for geological and technical expertise. The Company’s current personnel may not include persons with sufficient technical expertise to carry out the future development of the Company’s properties. There is no assurance that suitably qualified personnel can be retained or will be hired for such development.

The Company faces increased competition for equipment and experienced personnel from competitors with greater financial and technical resources.

The mineral exploration and mining business is competitive in all of its phases. The mining industry is facing a shortage of equipment and skilled personnel and there is intense competition for experienced geologists, field personnel, contractors and management, including from competitors with greater financial resources. There is no assurance that the Company will be able to compete successfully with others in acquiring such equipment or personnel.

There is no guarantee that the Company will be successful in its competition for productive mineral properties and financing with competitors possessing greater financial and technological resources.

The mineral exploration and mining business is competitive in all phases of exploration, development and production. The Company competes with a number of other entities in the search for and acquisition of productive mineral properties. As a result of this competition, the majority of which is with companies with greater financial resources than the Company, the Company may be unable to acquire attractive properties in the future on terms it considers acceptable. The Company also competes for financing with other resources companies, many of whom have greater financial resources and/or more advanced properties. There can be no assurance that additional capital or other types of financing will be available if needed or that, if available, the terms of such financing will be favorable to the Company.

There is no assurance that the Company will be able to obtain a leasehold interest to the land lot covering the Aukam Graphite Project on financially sound terms.

The land lot comprising the Aukam Graphite Project is owned by an unrelated third party, and the Company will need to obtain a leasehold interest to such land lot before it can commence mining operations. Under the laws of Namibia, the grant of a mining license guarantees access to the land where a mineral deposit is located. The financial terms of such access, however, need to be negotiated directly with the land owner. While the Company believes that it will be able to negotiate financially sound terms of such access when mining is commenced, there can be no assurance or guarantee that such terms will be acceptable to the Company.

There can be no assurance that the Company will be able to secure the renewal of the prospecting license or grant of a mining license on terms satisfactory to it, or that governments having jurisdiction over the Aukam Graphite Project will not revoke or significantly alter such license or other tenures or that such license and tenures will not be challenged or impugned.

The Company possesses the license to the Aukam Graphite Project allowing for prospecting operations, bulk sampling and pilot production (subject to ministry approval) in the license area, which expires on April 3, 2015. We submitted our application for an extension to our current Exploratory License on March 13, 2015 and are confident of it being renewed. The exploration license will be followed by a mining license, which cost is dependent on a number of variables that the Namibian Ministry of Mines will determine. We do not expect that the mining license will exceed $20,000 in annual cost. While the Namibian government has an interest in the license area being developed and the Company believes that it will be able to obtain necessary extensions on the prospecting license and grant of a mining license required to recommence mining operations, there can be no assurance that the Company will be able to secure the renewal of the prospecting license or grant of a mining license on terms satisfactory to it, or that governments having jurisdiction over the Aukam Graphite Project will not revoke or significantly alter such license or other tenures or that such license and tenures will not be challenged or impugned.

| 18 |

If environmental hazards are identified on the Aukam Graphite Project, it may have the potential to negatively impact on the Company’s exploration and development plans for the Aukam Graphite Project.

All phases of the Company’s operations will be subject to environmental regulation in the jurisdictions in which it operates. These regulations mandate, among other things, the maintenance of air and water quality standards and land reclamation and provide for restrictions and prohibitions on spills, releases or emissions of various substances produced in association with certain mining industry activities and operations. They also set forth limitations on the generation, transportation, storage and disposal of hazardous waste. A breach of such regulation may result in the imposition of fines and penalties. In addition, certain types of mining operations require the submission and approval of environmental impact assessments. Environmental legislation is evolving in a manner which will require stricter standards and enforcement, increased fines and penalties for non-compliance, more stringent environmental assessments of proposed projects and a heightened degree of responsibility for companies and their officers, directors and employees. The cost of compliance with changes in governmental regulations has the potential to reduce the viability or profitability of operations of the Company. The Aukam Graphite Project has in the past been subject to an environmental study. Additional environmental studies will, however, be required as the Company’s anticipated exploration and development programs unfold. It is always possible that, as work proceeds, environmental hazards may be identified on the Aukam Graphite Project which are at present unknown to the Company and which may have the potential to negatively impact on the Company’s exploration and development plans for the Aukam Graphite Project.

The price of the Company’s securities, its financial results and its exploration, development and mining activities may be significantly adversely affected by declines in the price of graphite.

The price of the Company’s securities, its financial results and its exploration, development and mining activities may be significantly adversely affected by declines in the price of graphite. Industrial mineral prices fluctuate widely and are affected by numerous factors beyond the Company’s control such as the sale or purchase of industrial minerals by various dealers, interest rates, exchange rates, inflation or deflation, currency exchange fluctuation, global and regional supply and demand, production and consumption patterns, speculative activities, increased production due to improved mining and production methods, government regulations relating to prices, taxes, royalties, land tenure, land use, importing and exporting of minerals, environmental protection, the degree to which a dominant producer uses its market strength to bring supply into equilibrium with demand, and international political and economic trends, conditions and events. The prices of industrial minerals have fluctuated widely in recent years, and future price declines could cause continued exploration and development of the Aukam Graphite Project to be impracticable. Further, reserve calculations and life-of-mine plans using significantly lower industrial mineral prices could result in material write-downs of the Company’s investment in the Aukam Graphite Project and increased amortization, reclamation and closure charges. In addition to adversely affecting reserve estimates and the Company’s financial condition, declining commodity prices can impact operations by requiring a reassessment of the feasibility of a particular project. Such a reassessment may be the result of a management decision or may be required under financing arrangements related to a particular project. Even if the project is ultimately determined to be economically viable, the need to conduct such a reassessment may cause substantial delays or may interrupt operations until the reassessment can be completed.

As our business grows, we will need to hire highly skilled personnel and, if we are unable to retain or motivate hire additional qualified personnel, we may not be able to grow effectively.

Although no assurance can be given, the Company contemplates that growth will occur as the Company implements its business strategies. The Company expects the expansion of its business to place a significant strain on its limited managerial, operational, and financial resources. The Company will be required to expand its operational and financial systems significantly and to expand, train, and manage its work force in order to manage the expansion of its operations. The Company’s failure to fully integrate new employees into its operations could have a material adverse effect on its business, prospects, financial condition, and results of operations. The Company’s ability to attract and retain highly skilled personnel in connection with its growth is critical to its operations and expansion. The Company faces competition for these types of personnel from other mining companies and more established organizations, many of which have significantly larger operations and greater financial, marketing, human, and other resources than does the Company. The Company may not be successful in attracting and retaining qualified personnel on a timely basis, on competitive terms, or at all. If the Company is not successful in attracting and retaining these personnel, its business, prospects, financial condition, and results of operations will be materially adversely affected.

| 19 |

The market price of the common stock may fluctuate significantly.

There was no quotation for the Company common stock until March 6, 2014. An active public market for the Company's common stock may not be sustained. The market price of the common stock may fluctuate significantly in response to factors, some of which are beyond the Company's control, such as competitors' results of operations, changes in earnings estimates or recommendations by securities analysts, developments in our industry, and general market conditions and other factors, including factors unrelated to our operating performance.

Issuance of additional shares of common stock or securities convertible into common stock may substantially dilute the ownership interests of our existing stockholders.

We may in the future issue our previously authorized and unissued securities, resulting in the dilution of the ownership interests of our common stockholders. We are currently authorized to issue one hundred million shares of common stock and ten million shares of preferred stock with such designations, preferences and rights as determined by our board of directors. Issuance of additional shares of common stock may substantially dilute the ownership interests of our existing stockholders. We may also issue additional shares of our common stock or other securities that are convertible into or exercisable for common stock in connection with the hiring of personnel, future acquisitions, future public or private placements of our securities for capital raising purposes, or for other business purposes. Any such issuance would further dilute the interests of our existing stockholders.

The outcomes of any legal action may have a material adverse effect on the financial results of the Company.

From time to time, the Company may be involved in lawsuits. The outcomes of any such legal actions may have a material adverse effect on the financial results of the Company on an individual or aggregate basis.

The Company does not anticipate paying any dividends on its common stock.

The Company has no earnings or dividend record and does not anticipate paying any dividends on its common shares in the foreseeable future.

Our common stock is considered a “penny stock” and, as a result, it may affect the ability of investors to sell their shares.

The SEC has adopted regulations which generally define "penny stock" to be an equity security that has a market or exercise price of less than $5.00 per share, subject to specific exemptions. The market price of the Company’s common stock may be below $5.00 per share and therefore may be designated as a "penny stock" according to SEC rules. This designation requires any broker or dealer selling these securities to disclose certain information concerning the transaction, obtain a written agreement from the purchaser and determine that the purchaser is reasonably suitable to purchase the securities. These rules may restrict the ability of brokers or dealers to sell such shares and may affect the ability of investors to sell their shares. In addition, since the Company’s common stock is currently quoted on the OTCQB, investors may find it difficult to obtain accurate quotations of the stock and may find few buyers to purchase the stock or a lack of market makers to support the stock price.

Failure to achieve and maintain effective internal controls in accordance with Section 404 of the Sarbanes-Oxley Act of 2002 could prevent the Company from producing reliable financial reports or identifying fraud. In addition, current and potential stockholders could lose confidence in the Company's financial reporting, which could have an adverse effect on the Company's stock price.

Effective internal controls are necessary for the Company to provide reliable financial reports and effectively prevent fraud, and a lack of effective controls could preclude the Company from accomplishing these critical functions. We are required to document and test our internal control procedures in order to satisfy the requirements of Section 404 of the Sarbanes-Oxley Act of 2002 (the “Sarbanes-Oxley Act”), which requires annual management assessments of the effectiveness of the Company's internal controls over financial reporting.

If we fail to maintain the adequacy of our internal accounting controls, as such standards are modified, supplemented or amended from time to time, we may not be able to ensure that we can conclude on an ongoing basis that we have effective internal controls over financial reporting in accordance with Section 404. Failure to achieve and maintain an effective internal control environment could cause investors to lose confidence in our reported financial information, which could have an adverse effect on our stock price.

Under the JOBS Act we have elected to use an extended period for complying with new or revised accounting standards.

We have elected to use the extended transition period for complying with new or revised accounting standards under Section 102(b)(1), which allows us to delay adoption of new or revised accounting standards that have different effective dates for public and private until those standards apply to private companies. As a result of this election, our financial statements may not be comparable to companies that comply with public company effective dates.

| 20 |

ITEM 2. PROPERTIES